Dunkies, Data, and Defensive Equilibrium

Humans like to believe in their own rationality. Markets, we are told, allocate efficiently. Firms optimize for productivity. Capital flows, inevitably, toward utility.

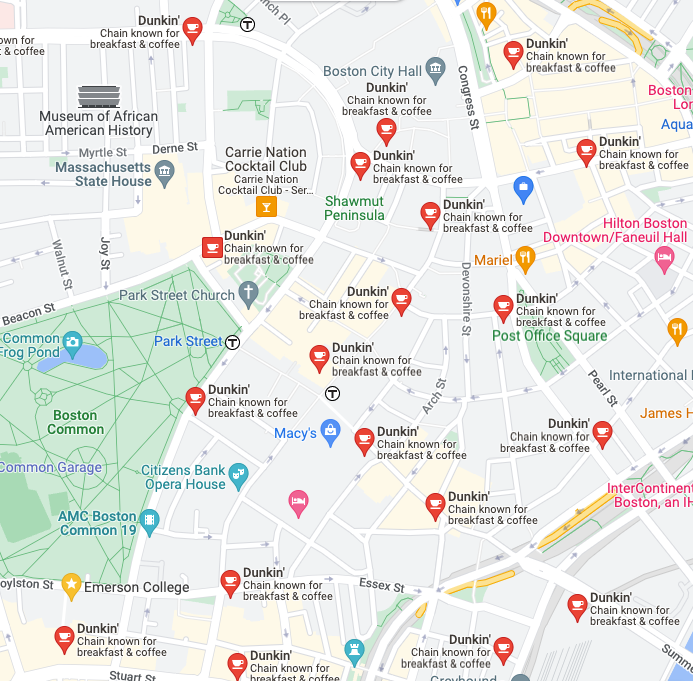

Yet we repeatedly observe clustering that appears inefficient: Dunkin’ stores across the street from one another. Mattress retailers on the same corner. Biotech companies converging on nearly identical AI positioning.

These are not market failures. They do not mean that Bostonians are buying two mattresses a day, or grabbing a cruller then an extra large and then three Parliaments. These configurations are equilibria.

Hotelling’s Law describes why. Imagine two vendors on a 100-yard beach. The socially optimal configuration is one at 25 yards and one at 75; that way, consumers never walk more than 25 yards. Utility is maximized for both producers and consumers.

But that configuration – while efficient for utility – is unstable. One vendor can move toward the center and capture more territory. The other must follow. Eventually both stand, back-to-back, at exactly 50 yards: inefficient for the beach, but stable for the vendors.

Nash equilibrium is often inefficient. It is stable because unilateral deviation from the competitive incentive structure is punished.

We mistake inefficiency for irrationality because we perceive a loss of utility. Competitive systems, however, frequently optimize for defensive stability rather than socially optimal scenarios.

In biotech, the center of the beach is not geographic. It is narrative.

Narrative as Boundary Selection

In Boundary Illusions, I argued that framing determines what a system can solve. In When the Levees Break, I argued that AI erodes institutional containment faster than governance can redesign it.

Our boundaries don’t operate by themselves without interaction. They’re all fighting for scarce resources under heavy uncertainty, especially now. Therefore, there’s another force shaping boundaries: competition under capital constraint.

Drug development remains long-cycle and capital intensive, averaging roughly $950 million over 12-15 years with single-digit-to-low-double-digit success probabilities. In restrictive funding environments, firms compete on two currencies: data and signal.

When robust data are available, the frame is grounded in measurable outcomes. But in early-stage discovery – where proof is sparse, continuing means staking tens of millions more dollars, and ROI might still be a decade away – signal density becomes a strategic asset.

In 2026, AI has become the highest-density signal available.

A proprietary reasoning engine implies scale, speed, defensibility, platform leverage, optionality. Adding in public or large-scale private repositories of data in biobanks, AI appears risk-mitigating and proactive. However, whether those optimistic implications are realized is secondary in the short term. What matters is that absence of AI carries immediate cost.

The incentives are straightforward:

- The reputational cost of appearing technologically obsolete is immediate.

- The partnership cost of lacking AI positioning is immediate.

- The capital-raising cost of narrative deviation is immediate.

- The integration, governance, and opportunity costs of adoption are deferred.

Under these conditions, clustering around a hyped technology is rational. In other words, no firm wants to be the vendor at 25 yards when capital markets are crowding the center.

We Have Seen This Before

This is not the first time biotech has clustered around a narrative center.

CRISPR created a similar gravitational pull. The underlying science was – and remains – transformative. But once Jennifer Doudna and others demonstrated the platform potential of the technology, firms rapidly expanded scope into multi-indication pipelines, rapid programmability, universal editability.

CRISPR has endured. However, we’re not freely editing organisms everywhere to cure disease and advance synthetic biology. The platform narratives did not all scale.

Capital eventually differentiated between:

- Firms that translated editing capability into validated therapeutic assets, and

- Firms whose surface area expanded faster than their clinical maturation.

The mid-2010s “platform biotech” wave followed a similar arc. Horizontal applicability across therapeutic areas, automation to facilitate scale, end-to-end discovery engines, integrated omics stacks, and synthetic biology toolkits like CRISPR together promised compounding advantage.

Some platforms survived by narrowing scope and integrating deliberately. Others discovered that declared platform breadth required managerial coherence, compute infrastructure, hardware, and capital reserves that outpaced their root systems. They found that their main selling point – end-to-end generalizability – was what ultimately became untenable to maintain.

In each cycle, the technology was real. What failed was not the capability of the technology; it was surface-area discipline, governance, and boundary maintenance under capital constraint.

AI is following a similar trajectory.

Surface Area and Selection

Narrative convergence has a structural consequence: surface area expansion. The major hype cycles in each case promise abstraction and generalizability, but fail to live up to their most idealized potentials.

In our current system, AI-first organizations often widen their declared scope, and these feel quite familiar: multi-indication platforms, horizontal data ingestion, end-to-end automation, cross-therapeutic applicability. Each additional claim presents both déjà vu and an expansion of the boundary of responsibility.

Surface area is not free.

A clinical-stage biotech with a $40–80M annual burn and 18–24 months of runway does not have indefinite integration capacity. Every additional therapeutic area, data vertical, or automation layer compounds managerial complexity, review cost, compute infrastructure, and regulatory exposure. That’s as true now as it was then.

Surface area expands geometrically. Revenue does not.

In capital-abundant environments, surface area can be subsidized by signal. In constrained markets, maintenance outpaces replenishment. Biotech is structurally capital dependent, and current conditions amplify that dependency.

This means that the failure mode will not be technical incapacity. It will be capital starvation induced by surface-area inflation.

High-surface-area firms without validated assets will discover that their narrative canopy expanded faster than their root systems. Capital markets tolerate delayed yield because of collective signal mechanisms. Those same markets do not tolerate indefinite canopy without harvest.

When signal density no longer compensates for burn, selection pressure intensifies.

The result will not be a broad rejection of AI. It will be a Darwinian shakeout.

Firms that optimized for height over yield will struggle to maintain themselves. Firms that converted narrative into durable assets – validated molecules, disciplined pipelines, explicit governance structures, scientific findings, resonant commercial narratives – will survive.

The correction won’t obliterate the surface, it will compress it.

After the Center

The durable organizations will not avoid the center of the beach. They will understand why they are standing there.

They will:

- Treat AI as boundary redesign, not boundary dissolution.

- Price governance as infrastructure, not overhead.

- Narrow declared scope until integration capacity matches ambition.

- Convert signal into fruit before expanding canopy.

In practice, this means narrowing before expanding. Converting signal into one validated program before declaring five. Using AI to kill programs earlier rather than to justify new ones. Surface area that grows without proportional asset maturation is not platform strength. It is balance sheet brittleness.

Markets reward acceleration. Selection rewards containment. The system is not irrational. It is optimizing defensively, until capital reintroduces discipline.

And when it does, the tallest trees with the fewest fruit will fall first, leaving the firms that stage-gate surface area expansion against validated asset conversion ratios.

Enjoy Reading This Article?

Here are some more articles you might like to read next: